November 1, 2021

Market Focus

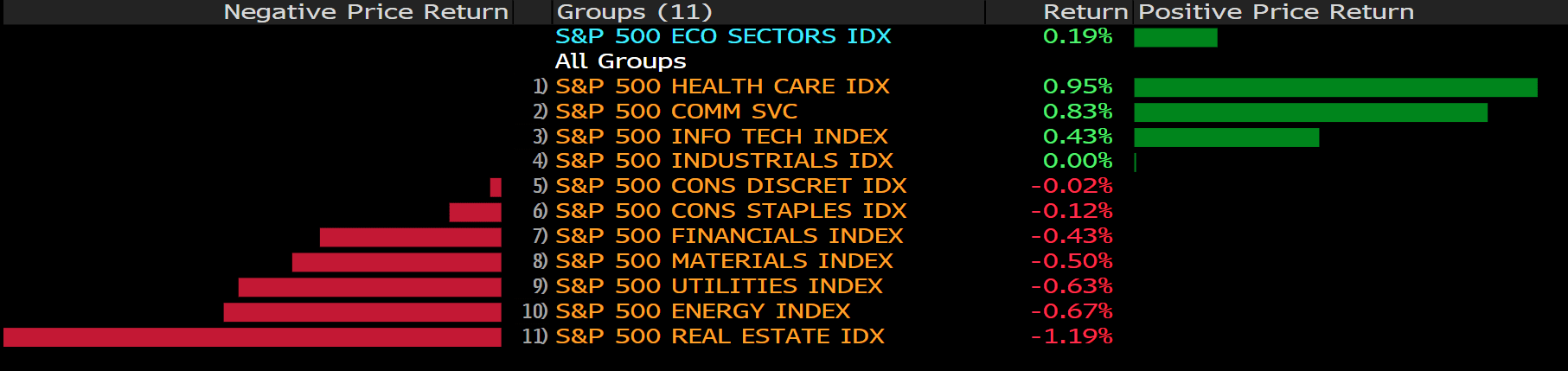

Stocks ended at records on Friday as investors digested disappointing earnings results from Apple (AAPL) and Amazon (AMZN) that came during an otherwise solid quarterly reporting season from many major companies. The S&P 500 set record intraday and closing highs. The index posted monthly gain of over 6.5% in October, or its best single-month advance since November 2020. The consumer discretionary, energy and information technology sectors outperformed during the month. The Nasdaq also eked out a fresh record level, even as a couple of heavily weighted technology giants saw shares dip.

Apple had seemingly avoided the chip shortage for months, but the company’s fortunes have now changed. On Apple Inc.’s quarterly earnings call Thursday, CEO Tim Cook was quick to tell investors and analysts that the company’s product shortages aren’t the result of a “fundamental error that we’ve made” and that its supply chain strategy didn’t create the current troubles.

Instead, he laid the blame on suppliers. While Apple designs its products in-house and relies on contract manufacturers like Foxconn Technology Group to assemble its devices, it’s dependent on hundreds of global suppliers to provide it with the parts and chips that make up an iPhone, iPad, Apple Watch or other device. If only one chip or part is in tight supply, Apple can’t build and ship that device. There lies the problem—not Apple’s scrutinized manufacturers in China, Cook seemed to imply.

It’s not surprising to see Cook defend Apple’s supply chain strategy. After all, he was the one who helped forge the partnership with Foxconn and build its supply chain empire two decades ago. If it were not for the current problems, Apple would have reported a record $90 billion for its fiscal fourth quarter. And instead of missing analyst expectations for total sales—as well as falling short in revenue from the iPhone, Mac and accessories—it probably would have had a clean sweep of beating Wall Street forecasts.

Main Pairs Movement:

The US dollar appreciated hugely on Friday as the market positions for the Fed’s meetings next week and amid higher US Treasury yield. The dollar index surged 0.83% at the end of the week, and the greenback beat all of its major rivals. The US Core Personal Consumption Expenditures accelerated 3.6% YoY in September, reaffirming the theory that the Fed will be forced to accelerate its monetary normalization plans, which, less than one week ahead of November’s meeting, has boosted demand for the USD.

The shared currency erased all of its gains against its rivals as the GDP figures appeared disappointing. The cable closed the day in the red, dropping 0.76% throughout the day. Commodity-linked currencies are also lost significantly against the greenback as well. And so does the USD/JPY pair.

Gold slid to $1783/ounce amid the broader dollar strength. Crude oil prices closed mixed, with WTI posted a modest gain to $83.28, and Brent dropped over 1% to $83.62 after Iran’s return to Joint Comprehensive Plan of Action (JCPOA), a nuclear agreement between Iran and some major countries, becomes possible.

Technical Analysis:

USDJPY (4- Hour Chart)

USDJPY gains positive traction after the release of the US PCE Price Index, trading at 114.0215. The US dollar revives as a strong pick up in the US treasury yields, boosting the demand for the greenback. From the technical perspective, USDJPY remains supportive on Friday after the pair trades above the midline of Bollinger Band. However, from a bigger outlook, the pair still maintains its bid tone as the October’s trend is still in the descending mood. Thus, it will be prudent to wait for a strong breakthrough. The pair will need to break above 114.699, the next resistance, in order to reverse its current trend. The RSI indicator has not reached the overbought territory, giving rooms for the pair to extend further north.

Resistance: 114.699

Support: 113.38, 112.57, 111.91

EURUSD (4- Hour Chart)

After the release of US inflation data, EURUSD push lower toward 1.1580 as the time of writing. From the technical perspective, EURUSD lost its upside momentum after attempting to contest the resistance at 1.1685 on Thursday. It can be viewed as a technical correction as the RSI indicator on the 4- hour chart is edging lower after reaching above 70, the overbought territory. The outlook of the currency pair turns bearish as it trades below the Simple Moving Averages. At the same time, bears are supported by the negative MACD. To the downside, the pair is expected to head toward the next immediate support level at 1.1524.

Resistance: 1.1624, 1.1685, 1.1735

Support: 1.1524

GBPUSD (4- Hour Chart)

GBPUSD is on the backfoot, trading below 1.3700, as the US dollar rebounds in the American trading session. From the technical aspect, the outlook of the currency pair remains downside as it falls within the lower bounce of Bollinger band and below the Simple Moving Averages. The RSI indicator returns below 50, suggesting that buyers remain hesitant when it comes to a steady advance. At the moment, the pair is heading to the next immediate support level at 1.3673; downside momentum continues to exist as the RSI has not yet reached the oversold territory, providing rooms for further southern move.

Resistance: 1.3735, 1.3835

Support: 1.3673, 1.3623, 1.3573

Economic Data

|

Currency

|

Data

|

Time (GMT + 8)

|

Forecast

|

|

CNY

|

Manufacturing PMI (Oct)

|

09:00

|

49.7

|

|

CNY

|

Caixin Manufacturing PMI (Oct)

|

09:45

|

50.0

|

|

GBP

|

Manufacturing PMI (Oct)

|

17:30

|

57.7

|

|

USD

|

ISM Manufacturing PMI (Oct)

|

23:00

|

60.4

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|